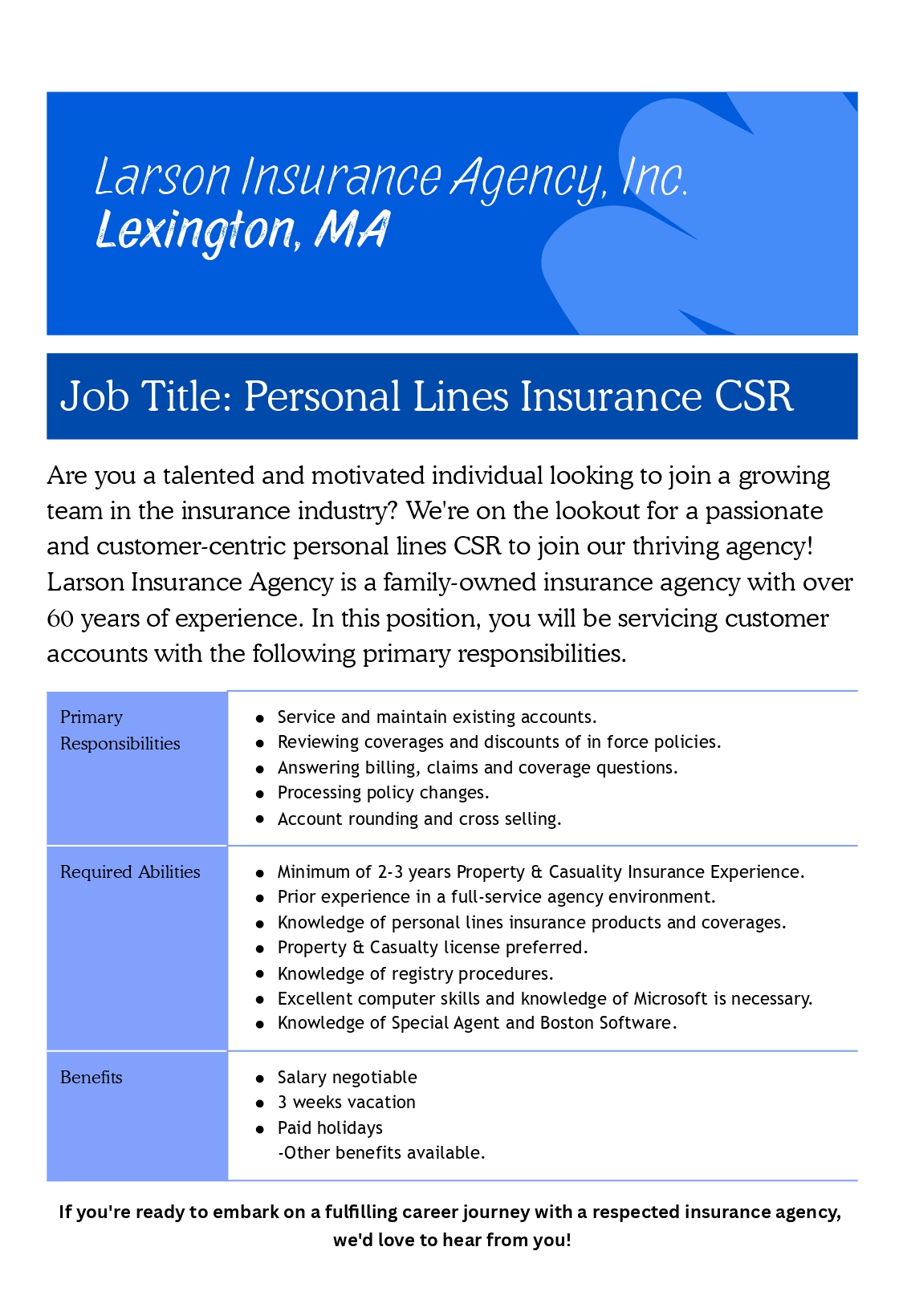

It’s a scenario many drivers know all too well: a quiet drive at dusk, a flash of movement in the periphery, and then—thud.

Animal collisions, particularly with deer, are more than just a startling road hazard; they are a massive part of the insurance landscape. In the United States alone, insurers process approximately 1.7 million animal collision claims annually. While that number has dipped slightly from previous years, the cost of repairs is hitting record highs due to the complex sensors and tech packed into modern bumpers.

If you’ve recently had a run-in with a buck or are just looking to be prepared, here is what you need to know about how these accidents interact with your insurance policy.

Does My Insurance Cover Hitting a Deer?

The short answer is: It depends on your coverage type.

- Comprehensive Coverage: This is the “gold standard” for deer accidents. Because hitting an animal is considered an unpredictable “act of nature” rather than a driving error, it falls under Comprehensive (often called “Other Than Collision”).

- Collision Coverage: This typically does not cover hitting the deer itself. However, if you swerve to miss the deer and hit a tree, guardrail, or another car instead, it becomes a Collision claim.

- Liability Only: If you only carry the state-mandated minimum liability insurance, your repairs will likely not be covered. Liability pays for damage you cause to others, not your own vehicle.

The Financial Ripple Effect

Even if you have the right coverage, there are a few financial hurdles to keep in mind:

| Factor | What to Expect |

| Deductibles | You will likely have to pay your Comprehensive deductible (often $250–$1,000) before the insurance kicks in. |

| Repair Costs | The average claim for an animal strike has climbed to over $4,000–$7,000, largely because a “simple” bumper replacement now involves recalibrating cameras and radar. |

| Rate Increases | Generally, a Comprehensive claim for a deer strike won’t spike your rates as much as an at-fault accident. Some states even have laws preventing insurers from raising premiums for “not-at-fault” animal collisions. |

5 Critical Steps After Impact

If the unthinkable happens, your priority is safety, followed by documentation for your claim.

- Move to Safety: Pull over, turn on your hazard lights, and stay in your car if it’s dark.

- Call the Authorities: Even if there are no human injuries, a police report is a vital piece of evidence for your insurance company to prove the damage was caused by an animal.

- Keep Your Distance: Never approach a downed deer. An injured animal is frightened and can be incredibly dangerous.

- Document the Scene: Take photos of the damage to your car, the road conditions, and—if possible—any hair or biological evidence on the car. This proves you actually hit the animal (Comprehensive) rather than an inanimate object (Collision).

- Check for Leaks: Before driving away, check for leaking fluid or a damaged radiator. A deer hit often causes “hidden” engine damage that can lead to a total engine failure if driven.

Pro-Tip: The “Don’t Swerve” Rule

It sounds counterintuitive, but experienced insurance agents and safety officials often advise that if a collision is inevitable, it is safer to brake firmly and stay in your lane rather than swerving. Swerving often leads to more severe “at-fault” accidents with oncoming traffic or fixed objects, and it can complicate your insurance claim by moving it from a Comprehensive to a Collision category.

Whether you’re driving through the wooded backroads or navigating the busier streets of your town, staying alert is your best defense. Since these accidents are often unavoidable, having the right coverage in place is the only way to protect your wallet from a sudden hit. Take a moment to review your policy today so you can drive with confidence, knowing you’re prepared for whatever runs across the road.